The Semiconductor Decade

- Apr 3, 2023

- 10 min read

Imagine being an executive at a car manufacturer with hundreds of millions of dollars in inventory when consumer demand is accelerating, but there is no way to fill orders due to an inability to get chips that might only cost $50. This is what was experienced during the pandemic. Automakers lowered their production estimates in the lockdown environment and canceled their semiconductor orders. Then car demand recovered, and automakers needed those cancelled orders. This “just-in-time” inventory approach combined with semiconductor production lead times that can take 3-6 months meant these companies were at a standstill. According to consulting firm AlixPartners, the chip shortage cost the global auto industry $210 billion in revenue in 2021.

These recent chip shortages have moved the industry into the spotlight over the past few years, and awareness has grown around two critical characteristics of semiconductors. First, they are integral to the modern economy. Semiconductors power almost everything in our daily lives and are vital to innovation in areas such as communications, computing, transportation and clean energy. And second, most leading-edge chips are sourced from East Asia (Exhibit 1), giving rise to geopolitical and supply chain concerns. These concerns have resulted in a global focus to bolster onshore manufacturing. The US passed the “CHIPS and Science Act,” the EU passed the “European Chips Act,” Japan announced a multi-billion-dollar initiative to boost its domestic chip industry and China cited the semiconductor industry as a key area of focus in its updated Five-Year Plan.

Short-Term Performance Challenges, Long-Term Value Creation

The Artisan Partners Growth Team is committed to finding reasonably valued franchises with accelerating profit cycles globally. One area of the market where the investment team have found a disproportionate number of companies that fit their investment criteria is the semiconductor industry. Over the years, they have enjoyed multiple successful long-term investment campaigns in semiconductor companies. The semiconductor industry within the MSCI AC World Index has experienced a return of 405% (Exhibit 2), more than 3X the broader index return over the last decade.

However, it is important to understand that the industry can experience performance challenges over shorter periods, such as 2022 (Exhibit 2) as the industry grappled with cyclical declines in demand for chips in end markets like PCs and mobile phones. The cyclicality of the industry is well-known and is a function of the fact that it can take three months to manufacture the most complex chips and an additional two to three months for the chips to make their way from the fabrication lines to end consumer devices. This lag, coupled with ebbs and flows in economic conditions, and optimization behaviors by different participants in the value chain, makes cycles inevitable. While many investors may be avoiding the industry for this reason, the investment team see this as an opportunity to participate in powerful profit cycles at attractive valuations being driven by investor pessimism.

Given the recent underperformance and general buzz around the industry, the team outlined their thesis for maintaining conviction in these investments. Among their main reasons are:

Consolidation and specialization contributing to secular profitability improvements

End market growth in new areas such as cloud computing and Internet-of-Things

Transformation of legacy industries (i.e., automobiles) made possible by increasing semiconductor content

Increasing returns (1) and chip proliferation (2 and 3) allowing companies to dedicate more of their margin to R&D investment, driving a virtuous cycle of growth and continued investment

1. Consolidation and Specialization

In the early days, semiconductor companies were vertically integrated and referred to as integrated device manufacturers (IDMs). However, the IDMs began breaking up around the turn of the millennium, and companies began specializing in two primary business models—designers (fabless) and foundries (fabs). Foundries manufacture chips while designers focus their efforts on product design, quality assurance, R&D, marketing and customer support.

Designers

Software plays a critical role in design for fabless companies, especially for digital chips whose architectural drawings are being completed at a nanometer scale and include billions of electrical components. As chips have become smaller, the overall cost and person production hours have increased significantly. It can take as many as 864,000 person days and $540 million to design a five nanometer (nm) chip—approximately double the time and money required to create five-year-old products (Exhibit 3).

Foundries

Once complete, the schematic is printed and handed off to a foundry for manufacturing. Taiwan Semiconductor Manufacturing Company (TSMC) is the dominant player with ~60% market share and higher for leading-edge technology. Outsourcing manufacturing allows designers to avoid the significant costs and risks associated with owning and operating plants which come at a price tag measured in billions of dollars. Constructing a new plant can take two-to-three years and costs roughly $10-$20 billion—more than a state-of-the-art aircraft carrier or nuclear power plant. TSMC is building two advanced fabs in Arizona with a total expected price tag of ~$40 billion.

The highly capital-intensive production process has six key steps requiring microscopic precision: wafer manufacturing, masking, etching, doping, testing and final assembly/packaging. Chips start from a straightforward raw material, sand, which is primarily made up of silicon dioxide. The sand is combined with carbon dioxide and melted down at high temperatures to form a thick cylindrical rod called a silicon boule. The boule is sliced into thin wafer disks—up to 300mm in diameter, <1mm thick—and is then covered by a uniform layer of photoresist material to render the chip’s surface light-sensitive. The wafer is subsequently exposed to extremely precise rays of UV light to develop the desired conductor structure—a process called lithography. This process is highly intensive as each chip can have hundreds of microscopic layers of transistors and electrical circuits. From there, the wafer undergoes a chemical or gas bath to reveal its patterns. The wafer is then bombarded with positive or negative ions to tune the electrical conducting properties. Once complete, up to tens of thousands of chips are sawed out of the wafer and packaged.

Improving Economics

Both businesses (designers and foundries) are incredibly intricate and capital-intensive, and specialization has allowed for companies to focus on their own niche areas of expertise. Designers have further specialized while manufacturers have scaled. At the same time, the industry has gone through massive consolidation (Exhibit 5), which has meaningfully improved profitability over the past 20 years when looking at metrics such as return on invested capital (ROIC).

Chip Proliferation

Advancements stemming from the semiconductor industry are felt in virtually every sector of the global economy. A large part of demand has historically been driven by the PC and smartphone end markets, but the rise of new applications, along with the transformation of existing markets, will continue to drive growth while diversifying the industry’s exposures (Exhibit 6). The investment team believe these trends will be key drivers in doubling (or more) the industry’s revenue by the end of this decade.

2. Emerging Growth Markets

Cloud Computing

Cloud computing is the third major computing paradigm after mainframe and client-server. Cloud computing uses the internet to enable access to distributed storage, processing power, databases, analytics and software applications. Companies leveraging cloud resources can access the computational assets needed without purchasing and maintaining a physical, on-premise IT infrastructure. This frees up capital and resources to innovate and scale faster, lower organizational costs and provide better data security. Data centers play a critical role in cloud infrastructure, and the processing power embedded within them comes from semiconductor chips.

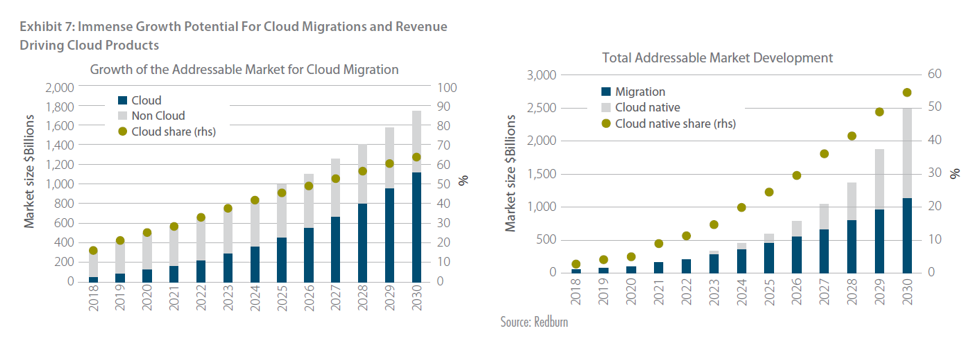

The cloud transition has been going on for over a decade, but it is still early considering less than 30% of enterprise workloads are in the cloud (Exhibit 7). On-premise workloads are costly to maintain, and enterprises are still early in transitioning. Meanwhile, the opportunity to add additional services after making the cloud migration is immense. Conducting analyses to gain insight and make predictions (e.g., artificial intelligence, machine learning, deep learning) are made accessible through the cloud. Both trends are demand tailwinds for several of the portfolio's holdings, which design the chips serving as the “brain power” for these technological leaps.

Advanced Micro Devices is a holding in the Global Opportunities Strategy; the company’s datacenter CPUs are used in the cloud service providers (CSPs) servers. In addition to the broader secular tailwind from cloud adoption, the company has both a performance and pricing advantage over Intel, which the team believe will enable it to capture additional market share for the foreseeable future. Despite the waning macroeconomic backdrop causing weakness in the company’s PC end market (~40% of revenue in 2021) over the near-to-intermediate term, they believe this high-quality franchise’s durable profit cycle drivers will enable it to deliver meaningful growth over the next three-to-five years.

Internet of Things (IoT)

The “Internet of Things” is a broad term that refers to the growing network of connected devices that can collect and exchange data in real time. These semiconductor-powered devices impact virtually every area of society. Transportation, health care, infrastructure, manufacturing, and the consumer end markets utilize them to sense, analyze and produce insights enabling more informed decisions. Within health care, monitoring devices can collect patient data in real time and use algorithms to analyze the results. For example, diabetics are benefiting from wearable devices that continuously monitor glucose levels and alert patients when levels are problematic. Within industrials, companies are benefitting from the increased use of sensors and robotics to automate manufacturing processes to scale production, increase product quality, drive operational efficiencies and improve safety. The pace of growth over the past six years has been extraordinary (>3X, Exhibit 8), and some estimate these devices could more than double over the next four years.

Lattice Semiconductor, a holding in the Global Discovery Strategy is a fabless vendor of field programmable gate array (FPGA) chips—hardware circuits customers can program/configure after manufacturing. Lattice’s FPGA chips are used in personal computers, 5G infrastructure, routers and switches, servers, industrial IoT devices, factory automation, automobiles and TVs to name a few. The company has refreshed its FPGA products in the small/low power segment of the market, carving itself a niche behind the two market leaders Xilinx and Intel. The product set is now more focused on addressing high return-on-investment use cases centered around small (low-end) and power-efficient applications—a rapidly growing market to which Lattice brings unique intellectual property versus a broad set of peers in the semiconductor industry. In addition to providing FPGA chips to data centers and new 5G infrastructure—particularly compelling opportunities given these end markets should continue benefiting from strong secular tailwinds—the investment team believe the company is well-positioned to tap into low power/reprogrammable chips as well as industrial and automotive end markets.

3. Transformation of Legacy Markets

Autonomous and Battery-Electric Vehicles

Semiconductor content in vehicles (i.e., cost + units) has increased rapidly as cars become more technologically advanced. Most new vehicles are packed with chips enabling Bluetooth®, vehicle diagnostics, climate control, navigation systems and advanced driver assistance (ADAS)—which uses devices for automatic emergency braking, lane departure warning and correction, blind spot detection and traffic sign recognition to increase driver safety. ADAS is the first step towards realizing autonomous vehicles.

Nearly every major car manufacturer is developing autonomous driving technology today. The level of automotive automation is commonly classified by levels “L0 to L5.” Today, most cars classify as L0 to L2 with L2 meaning the vehicle can perform some steering and acceleration. As autonomous driving technology progresses and vehicles move towards the L5 (fully autonomous) stage, estimates suggest cars will require >2.5X the amount of semiconductor content.

Another tailwind to semiconductor demand is the transition to battery electric vehicles (BEVs), which require >2X the value of semiconductor content than their internal combustion engine (ICE) counterparts. Examining Exhibit 10, BEVs require ~$1,300 of semiconductor content per vehicle. This is primarily due to the cutting-edge power technologies needed to support the electrification of the powertrain, extend the driving range and reduce charging time.

One example is silicon carbide (SiC) chips. These chips can operate at higher voltages, temperatures, and frequencies than traditional silicon-based chips. While SiC chips have been around for decades, there was no need for their high-power application until EVs emerged as a critical driver of demand. SiC chips enable high power voltage conversation more efficiently, increasing driving range and reducing charging time, two critical factors driving mass adoption of EVs.

ON Semiconductor, a CropSM holding in the Global Discovery Strategy, is a leading designer and manufacturer of chips used for power management and image sensors. The investment team believe it is well-positioned to benefit from growing demand across several end markets. From a BEV standpoint, ON is the leading producer of silicon carbide chips (SiC), which have a combination of physical characteristics that provide power conversion, size, and temperature advantages over silicon and can amount to up to 10% savings on battery cost and extend range by a similar amount. SiC chips allow for lighter, longer-range electric vehicles and enable efficient, fast-charging stations. Range is a key competitive advantage for BEV automakers, and they expect ON’s SiC chips to be in high demand as BEV volumes ramp. Meanwhile, ON’s chips are also used in factory automation, renewable energy infrastructure, machine vision and imaging and depth sensors critical for ADAS (and eventually autonomous vehicles).

Allegro MicroSystems, a CropSM holding in the U.S. Small-Cap Growth Strategy, is a fabless semiconductor supplier of magnetic sensors and power integrated circuits primarily for the automotive and industrial industries. Allegro is the market leader in magnetic sensors with an even higher share in automotive where its chips are used to precisely measure motion, speed, position, voltage, and current in a variety of applications. The company’s power integrated circuits and regulators are used to drive high temperature and high voltage motors which are well suited for EV/HEV’s, auto LED lighting, and data centers.

4. Increasing Returns Drive R&D Investment

Manufacturing chips with exponentially more transistors requires increasing precision, and this increasing complexity makes state-of-the-art semicap equipment critical. Perhaps the best example of semicap equipment innovation and R&D requirements is the ultraviolet (EUV) light lithography machines developed by ASML. Lithography is a critical, yet difficult, step in the manufacturing process. EUV is used to pattern the finest details on the most advanced microchips, which plays an important role in packing more transistors onto a single chip. ASML spent 17 years and ~$9 billion developing its EUV technology, while its competitors made no such investment, opening the door to ASML having a monopoly in the EUV market. A state-of-the-art EUV machine is made up of thousands of components, costs upwards of $200 million and requires multiple jumbo jets to be delivered.

Total industry capital expenditure spending has grown to $150 billion in 2021. The next innovations and manufacturing leaps will likely require increasing amounts of R&D spend. As the team have discussed earlier, despite these rising CapEx costs, industry consolidation has led to companies experiencing increasing levels of profitability while increased chip proliferation is driving revenue growth. They believe this sets the stage for increasing returns that will support rising R&D investments and continued innovation.

Conclusion

The semiconductor industry has always been inherently cyclical, given the volatility around end market demand and resulting inventory builds. While the investment team have made the case that increased chip content is introducing more secular end market exposure, there will likely continue to be an aspect of cyclicality to this industry. However, chip demand will continue to move upwards, producing higher highs and lower lows through future cycles. Rather than try to market time these cycles, they would rather remain patient and hold these companies for the long term.

Performance in 2022 was challenging for the industry as valuations were elevated and companies were working through increased inventory levels. But valuations for the semiconductor industry have returned to more long-term averages which the team believe is an attractive starting point for investors with a long-term view.

Please refer to the disclaimer below.

Comments